Executive Summary

Executive Summary

This report models a worst-case but commercially grounded scenario: the effective closure of the Strait of Hormuz and the Persian Gulf’s seaward outlet from May 1, 2026 through December 31, 2027, with no reliable return of normal merchant shipping during that period.

What that means in plain terms is simple and brutal: one of the world’s most important economic arteries goes dark—and stays dark long enough that the global system can’t just “wait it out.” It has to rewire itself.

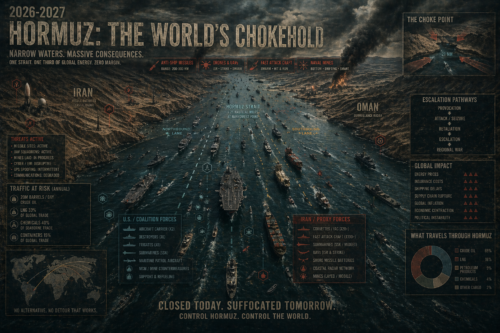

The scale of disruption is hard to overstate. In 2025, roughly 20 million barrels per day of oil—about a quarter of global seaborne oil trade—moved through Hormuz. At best, only 3.5 to 5.5 million barrels per day can be rerouted via pipelines through Saudi Arabia and the UAE. The rest doesn’t magically find another path; it becomes a constraint that ripples outward through prices, logistics, and policy.

Gas is even less forgiving. Around one-fifth of global LNG trade, largely from Qatar and the UAE, transits the Strait—and unlike oil, there is no meaningful maritime workaround. When those flows stop, they don’t detour; they disappear from the seaborne market.

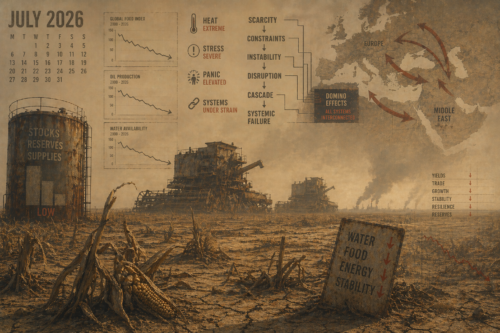

Fertilizers quietly complete the triad. About one-third of global seaborne fertilizer trade passes through Hormuz, with the Persian Gulf region heavily concentrated in urea exports. That places over 10 million tonnes of urea-equivalent supply at immediate risk, with knock-on effects that extend well beyond shipping into agriculture and food systems.

In the first phase—measured in weeks to months—the response is reactive and improvised. Governments release strategic stocks, ration supply, and scramble for alternatives. Shipping companies impose surcharges or withdraw entirely. Cargoes are rerouted through improvised land bridges and secondary ports, often inefficiently and at high cost. The system doesn’t collapse, but it grinds.

By late 2026, a second phase emerges. The shock is no longer treated as temporary. Trade flows stretch across longer distances, increasing shipping demand in some corridors even as others go idle. Buyers begin to shift away from Gulf-dependent supply chains—especially in LNG and fertilizers—not because it’s efficient, but because it’s survivable. Governments intervene more deeply, shaping markets through subsidies, controls, and procurement.

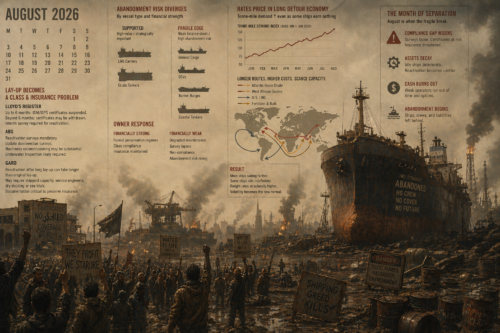

By 2027, the effects harden into structure. What began as disruption becomes redesign. Supply chains migrate. Contracts are rewritten around persistent risk. Entire categories of shipping—especially older, lightly financed vessels—face rising odds of lay-up, abandonment, or scrapping, while strategically critical fleets remain supported. The global system adapts, but not cleanly: it becomes more fragmented, more expensive, and more state-directed.

The key point is this: the most lasting impact of a prolonged Hormuz closure is not the initial price shock. It is the slow, uneven reconfiguration of global trade—energy, food, and shipping alike—around the absence of a route the world previously assumed would always be there.

May 2026 Under a Full Hormuz Closure

Month-by-month is cleaner here, so the right way to do this is to start with May 2026 as its own assessment. In practical terms, May is not “the first shock” anymore. It is the first month when emergency measures meet hard physical limits. By late March and early April, official and quasi-official trackers were already showing that traffic through Hormuz had fallen to a near standstill, oil supply had taken the largest disruption on record, and fertilizer, LNG, and freight costs were transmitting the shock well beyond the Gulf. The key point for May is this: shipping is the mechanism, but the main story is broader—oil and distillate tightness, LNG replacement limits, urea procurement stress, fiscal strain in importers, and the beginnings of politically visible cost-of-living backlash. Official baseline forecasts from EIA and the IMF still assume disruptions ease by mid-2026, so a true full-closure May is, by definition, worse than their central cases.

What May is actually about

For May, the most useful mental model is not “everything stops,” but “the world starts triaging.” WTO/AXSMarine and UNCTAD data show outbound crude, LNG, and fertilizer flows from the Gulf collapsing to near zero or near-zero visibility, while UNCTAD says daily ship transits through the Strait averaged 129 before the conflict and 6 in March, a roughly 95% drop. At the same time, the WTO’s methodology note is important: AIS-based trackers can understate actual traffic when AIS is switched off, so the right phrasing is “near halt,” not “literal zero.” In other words, May is a month of deep disruption and forced rerouting, but also of uncertainty, opacity, and exceptions.

Operationally, alternative corridors exist, but they are messy. Maersk’s April contingency architecture routes cargo through Jeddah, Khor Fakkan, Fujairah, Sohar, Salalah, and Aqaba, then onward by road or rail; Hapag-Lloyd said on April 8 that it would still avoid Hormuz because it was not clear whether any announced opening would hold. So in May, the visible logistics pain is likely to be congestion, booking restrictions, inland bottlenecks, higher insurance and transport charges, and prioritization of food, medicine, and time-sensitive cargo, not a total disappearance of trade. That matters for media and public opinion because people experience this as “things are available, but slower, costlier, and less reliable.”

Sector pressures in May

On oil, May is the month when stock releases are still cushioning the blow, but not solving it. The IEA says almost 20 mb/d of crude and products moved through Hormuz in 2025, equal to about 25% of global seaborne oil trade, while only about 3.5–5.5 mb/d can be rerouted through Saudi and UAE pipelines under current conditions. The IEA also reported that global oil supply fell by 10.1 mb/d in March, that Middle East and feedstock-constrained Asian refineries had cut runs by around 6 mb/d in April, and that early-April flows through the Strait were still severely restricted. EIA’s April forecast only gets May shut-ins down to 6.7 mb/d because it assumes the conflict does not persist past April; under a full-closure May, that easing assumption breaks. So the May oil story is not just “high crude.” It is persistent product tightness, especially in middle distillates and aviation fuels, plus continuing freight inflation.

On gas and LNG, May is harsher than oil because the substitution tools are weaker. The IEA says about 93% of Qatar’s and 96% of the UAE’s LNG exports transit Hormuz, equal to roughly 19%–20% of global LNG trade, and there is no alternative seaborne route for those volumes. EIA says U.S. LNG exports were already 17.9 Bcf/d in March, near peak capacity, meaning the world’s main swing exporter has only limited room to do more. That is why May is less about literal home-heating emergencies in Europe—Europe is entering the warmer season—and more about storage refill, industrial gas competition, and price pressure. Asia remains the first-order exposure because almost 90% of LNG exported through Hormuz in 2025 went there, while Europe’s exposure is more indirect via global price competition. A related immediate risk is aviation fuel: AP reported IEA chief Fatih Birol warning that Europe might have only around six weeks of jet fuel left if supplies remained blocked. So for May, jet fuel and flexible LNG cargoes look more acute than household heating.

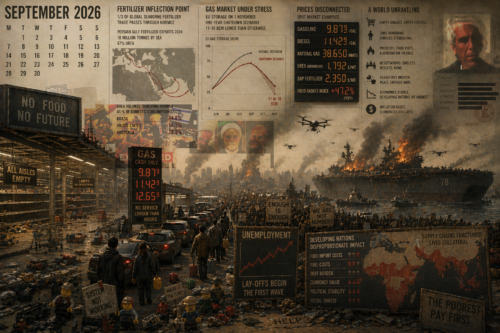

On urea and agriculture, the timing matters. UNCTAD says about one-third of global seaborne fertilizer trade passes through Hormuz and that the Persian Gulf region shipped 16 million tonnes of fertilizer by sea in 2024, of which 67% was urea. That means May is primarily a procurement and subsidy month, not yet a harvest-collapse month. Governments are already acting defensively: India in March moved fertilizer into the natural-gas priority list to protect domestic production, and in April approved nutrient-based subsidy rates for the 2026 kharif season. So the immediate May risk is prompt urea availability, tender failures, higher working-capital needs, and earlier state intervention, especially in import-dependent economies. The agricultural damage comes later if May and June procurement fails; in May itself, the thing to watch is whether buyers can still secure product, not whether yields have already collapsed.

Politics, public mood, and the May calendar

In political and geopolitical terms, May is a month of nervous holding patterns. The IMF’s regional update still assumes trade and production disruptions fade by mid-2026, but it also says the uncertainty is exceptionally high and that the impact on directly affected Gulf exporters could be severe even under a short-lived scenario. UNCTAD’s April note says the Strait remains “practically closed,” with slowing trade growth, higher inflation risk, weaker developing-country currencies, and higher external borrowing costs. That means the key May political divide is between governments trying to tell voters “this is manageable” and households starting to believe “this is becoming structural.”

Public mood is already shifting. AP reports that fuel protests in Ireland were serious enough to trigger a confidence vote, and also describes Europe as divided as rising energy prices spill into foreign-policy arguments. In the United States, AP reports March retail sales were flattered by a jump in gasoline spending, while consumer sentiment fell sharply as households absorbed higher fuel costs. So the May public-opinion picture is not yet one of generalized panic; it is a transition from abstract geopolitical anxiety to household-cost anger, especially around fuel, freight, and visible shortages such as airport disruption or delayed food logistics. Migration is still a second-order channel in May: the real near-term risk is not mass movement out of the Gulf next week, but economic stress in poorer importers that can later translate into displacement if food and fuel affordability worsens.

As for slated events, the most market-relevant one is the OPEC+ meeting on 3 May 2026, not an election. OPEC’s own April 5 statement says the eight countries will meet monthly and next reconvene on 3 May. EIA’s next STEO is due 12 May 2026, and the IEA’s next Oil Market Report is due 13 May 2026. Those three dates matter more for price expectations and policy signaling than any public election in the immediate week ahead. On elections, the publicly visible IFES ElectionGuide calendar shows Scotland and Wales voting on 7 May, with other May polls including Cabo Verde and Cyprus later in the month, while Lebanon’s 10 May parliamentary election is listed as postponed. Those are politically relevant, but none is likely to move the physical Gulf supply story the way OPEC+, truce durability, or emergency-energy policy would.

What is becoming scarce and what could still surprise people

The scarcities building into May are fairly clear. The first bucket is jet fuel and middle distillates, because product markets were already extremely tight in April. The second is prompt LNG flexibility, especially for Asian buyers. The third is prompt urea and fertilizer finance, particularly where governments do not have the balance sheet to subsidize or pre-buy. The fourth is cheap logistics capacity: even when cargo moves, it increasingly moves via more expensive and slower substitute corridors. And the fifth, often missed, is fiscal room in poorer importers, because UNCTAD and the IMF both emphasize that high debt, weaker currencies, and rising external borrowing costs reduce governments’ ability to cushion households.

The black swans for May are not movie-script events; they are uglier and more ordinary. One is that markets may still be underpricing a longer disruption: the IMF says financial markets have remained broadly orderly so far, but may not have fully priced a decisively adverse turn. Another is that the data themselves may understate residual or “dark” traffic, which means apparent calm in one indicator can hide unstable workaround trade. A third is policy interaction: if the closure persists, a bad monsoon outlook in India, or a breakdown in fertilizer subsidy capacity in poorer importers, would turn an energy shock into a more obvious food-security shock much faster. And the structural shift already beginning in May is simple: more state intervention, more long-haul substitution, more preference for out-of-Gulf export routes, and a more permanent risk premium on energy, fertilizer, and freight. May is the month when people stop asking whether the shock is real and start asking how long they can afford it.

This assumes a prolonged U.S.–Iran standoff with repeated truce breaches, partial resumptions, renewed interruptions, insurance dislocation, and persistent uncertainty around Hormuz, not a clean one-off shock and not a smooth return to normal. The key analytical mistake to avoid is treating this as “just an oil price story.” It is three different crises layered together: price shock, physical scarcity, and logistics paralysis. Those do not move in sync. Sometimes price spikes before shortages. Sometimes cargo exists but cannot move. Sometimes governments can fund imports but cannot secure molecules, ships, credit, or political calm.

June is the month of violent repricing. The first-order reaction is in oil, LNG, freight, insurance, and anything with Gulf exposure, but the deeper issue is that almost nobody knows whether this is a three-day panic, a three-week disruption, or the beginning of a semi-permanent harassment regime. Markets initially price the optimistic version and then slowly discover they were being sentimental idiots.

Oil rockets first because it is the fastest market to express fear. But even here, the distinction matters: there may still be plenty of oil in the world while there is suddenly much less oil that can clear to the right buyer at the right time through the right route under insurable conditions. Shipping schedules begin to break before supermarket shelves do. Refiners start triaging grades. Asian buyers, especially the ones most dependent on Gulf barrels, move aggressively to secure alternatives. Europe is less directly exposed on crude than Asia in some segments, but gets hit through product markets, freight, gas competition, and generalized panic.

LNG becomes the stealth killer in June because the public conversation lags reality. Oil gets headlines; gas gets the social consequences. Buyers in Asia start overbidding to secure cargoes. Europe immediately faces the ugly arithmetic that storage levels in summer matter far more under this scenario than the public realizes. A hot June also worsens power demand and cuts margin for error. Urea and fertilizer markets begin to seize up not because farmers instantly stop planting, but because traders, importers, and governments realize they may be heading into a period where nitrogen is no longer reliably available at tolerable cost.

Politically, June is the month when governments try to sound calm while quietly improvising. China is cautious, opportunistic, and deeply alert. It does not want a global collapse, but it absolutely will exploit dislocation to improve its buying position, deepen leverage with suppliers, and present itself as the adult in the room. Europe moves into emergency coordination language. Washington oscillates between deterrent posture and domestic political panic. Public opinion is still fluid at this stage; most populations interpret the crisis as either “another Middle East mess” or “another inflation event,” not yet as a structural break.

July is when the crisis stops being a market story and becomes a systems story. Inventories, hedges, and floating cargoes buy a little time, but the commercial machinery underneath begins to jam. Tanker availability tightens. Crewing stress rises. War-risk insurance and compliance reviews slow everything. Ports outside the Gulf begin seeing schedule distortions, bunching, and slot stress. What looked like a regional disruption starts turning into a global shipping inefficiency tax.

In oil, the world is now burning through its psychological comfort faster than its physical reserves. Spare capacity exists in theory, but not all spare capacity is usable at speed, and not all replacement barrels match refinery needs. Strategic reserves can soften panic but not fix route dependence. Refiners start making uglier choices: lower runs, different slates, narrower margins, or higher prices passed straight through. Diesel and fuel oil become especially politically sensitive because they bleed into freight, agriculture, backup generation, and basic goods.

July is also when fertilizer anxiety spreads into agriculture planning. The northern hemisphere is not instantly starving, but procurement calendars start to bend. Import-dependent states in Africa become nervous much faster than richer economies because they do not have the same fiscal space, buffer inventories, or currency credibility. Governments that already run fragile subsidy regimes start facing a brutal choice: subsidize food, subsidize fuel, subsidize fertilizer, or preserve the currency. They cannot do all four for long.

Media narratives fragment. Financial press talks about inflation and commodities. Mainstream politics talks about pump prices and “stability.” Online discourse becomes deranged in the usual way: conspiracies, election framing, anti-war sentiment, anti-immigrant opportunism, and bizarre certainty from people who have never seen a shipping schedule in their lives. Public opinion in Europe begins to harden around cost-of-living fatigue. In the U.S., the issue starts entering midterm framing through inflation, gasoline, “competence,” and the broader sense that the governing center is unstable and overextended even when nobody can quite agree on why.

August is where the danger of false stabilization appears. There may be partial resumptions, temporary corridors, tactical truces, or selective movement under escort or heavy conditions. Markets may briefly exhale. This is exactly the moment to distrust the calm. Under a repeated-breakdown scenario, August is not normalization; it is a demonstration that every restart is brittle.

The commercial world starts repricing not just risk but reliability. Long-haul contract structures change. Buyers prefer secure, boring suppliers over cheaper exposed ones. Freight premiums embed uncertainty. Insurers and lenders become more conservative. Some importers overbuy when they can, which worsens volatility for everyone else. That inventory hoarding becomes its own multiplier. The result is that even if physical flows improve somewhat, prices and logistics remain ugly because no one trusts continuity.

Europe in August becomes obsessed with gas storage, and for good reason. A mild summer and successful refill campaign can preserve winter survivability; a hot summer, repeated LNG interruption risk, or Asian bidding war makes the whole continent feel one bad month away from another energy-political crisis. Heavy industry in Europe starts gaming shutdown scenarios again. Chemicals, fertilizers, ceramics, metals, paper, and other heat-intensive sectors do the grim spreadsheet work of asking whether they are viable through winter at all.

China’s position becomes more interesting. It has more state capacity, more tolerance for industrial redirection, more coal fallback, and more willingness to use stockpiles and directed finance. It can weather pain better than many peers, but that does not make it immune. Gas-sensitive coastal industry still gets squeezed. Export competitiveness becomes a geopolitical weapon if China can secure energy inputs more effectively than rivals. Beijing also watches for a chance to broker language, posture as stabilizer, and quietly extract concessions from everyone involved.

September is when the crisis hits political metabolism. Summer narratives give way to autumn realities. Businesses stop hoping it will all pass and start cutting plans for Q4 and Q1. Households see that this was not just a spike in petrol and a few scary headlines. Heating anxiety starts entering public conversation in Europe and parts of Asia. Food affordability concerns become more visible in lower-income import-dependent countries. Governments that relied on temporary subsidies discover that temporary has become structural.

In oil, the market may no longer be at its most panicked price, but the macro damage broadens. High energy costs seep into transport, food processing, fertilizers, plastics, construction inputs, and municipal budgets. Central banks face the familiar nightmare: inflation that is externally driven, socially painful, and politically impossible to ignore, but tightening into it risks breaking already-weak labor markets. Stagflation talk returns, and this time it is not just pundit cosplay.

For Africa, September is the month where divergence becomes stark. Energy exporters may see revenue windfalls, though often with corruption and distributional distortion. Energy and food importers, especially those with weak currencies, heavy debt service, and limited fiscal room, face genuine macro stress. Fertilizer shortages and higher import costs do not always show up instantly in famine language, but they show up in lower planting intensity, weaker expected yields, more expensive food, and more combustible politics. Urban unrest risk rises where fuel, bread, and transport are tightly linked in the public mind.

Migration channels begin to matter more by September, not because masses move overnight from one shock, but because multiple pressures stack: food inflation, subsidy cuts, blackouts, conflict opportunism, and labor market erosion. The Mediterranean conversation in Europe starts to shift from border rhetoric to social stress, municipal burden, and the ugly politics of “capacity.” Even modest increases in flows can have outsized political effect when electorates are already angry, tired, and primed for scapegoating.

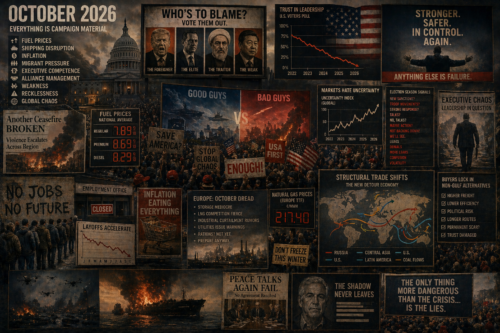

October is the month where the U.S. midterm cycle starts feeding back into the crisis rather than merely commenting on it. Everything becomes campaign material: fuel prices, shipping disruption, executive competence, alliance management, inflation, migrant pressure, “weakness,” “recklessness,” “global chaos,” the lot. The U.S. electorate, already operating on a level of emotional overclocking that would get a lesser civilization confiscated by adults, processes a structurally complex global supply crisis as a morality play with villains conveniently color-coded for domestic use.

That matters because October can produce policy noise even without coherent policy change. Threats, promises, leaks, contradictory signals, performative toughness, and election-season signaling all increase uncertainty premiums. Markets do not need actual regime change or dramatic constitutional melodrama to panic; they only need to suspect that the executive center cannot produce a stable line. Hint accepted: the issue is not one man’s biography but the broader fact that U.S. political continuity increasingly feels contingent, theatrical, and open to bizarre discontinuities.

In Europe, October becomes a referendum on whether summer preparation was enough. If storage is strong and weather mild, governments can limp into winter with high prices but manageable panic. If storage is mediocre, LNG competition remains fierce, and industrial curtailment rumors spread, then October becomes the month of preemptive demand destruction. Firms delay output. Utilities warn. Governments whisper about rationing without using the word. Public opinion shifts from annoyance to low-grade dread.

This is also the month when structural trade shifts become visible. Buyers lock in non-Gulf alternatives for longer duration. Russia, Central Asia, the U.S., West Africa, Latin America, and even coal supply chains gain strategic weight in distorted ways. None of this is clean. Substitution is partial, costly, and politically messy. But October is when the world begins to internalize that even if Hormuz does not remain fully shut, trust in that route has been damaged, and trade patterns may not snap back.

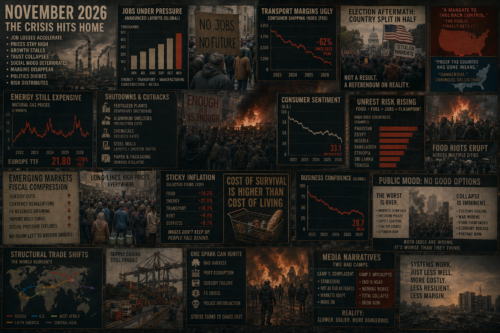

November is where the accumulated crisis shows up in jobs and social mood. Energy-intensive sectors that spent summer hedging and autumn waiting begin announcing layoffs, temporary shutdowns, shorter hours, or investment delays. Transport margins are ugly. Smaller firms crack before larger ones. Emerging-market importers face fiscal compression. Richer countries can borrow more, but even they cannot subsidize everything forever without political backlash.

In the U.S., the election outcome matters less here than the fact of intensified legitimacy conflict around the outcome. Half the country will interpret results as proof that the public has finally understood the danger; the other half will interpret them as proof that the country has gone fully insane. Either way, November does not produce calm. It produces a more partisan reading of the same external crisis. Consumer sentiment and business confidence remain weak because politics cannot lower the price of molecules by screaming at A.I. memes

For Africa and parts of South Asia, November can be genuinely dangerous. Governments with weak FX reserves and large food import bills may be forced into sharper subsidy cuts, exchange-rate moves, or arrears. Unrest risk is highest where urban populations are concentrated, informal labor is dominant, and food and transport costs are politically fused. Not every country cracks, obviously, but the probability distribution thickens. One bad harvest signal, one port bottleneck, one subsidy failure, one police overreaction, and a “manageable stress” story can turn into riots very quickly.

Media narratives by November begin polarizing into two bad camps. One insists the worst is over because markets are no longer at peak panic. The other insists total collapse is imminent. Both are lazy. The more accurate reading is nastier: the world may have moved beyond acute shock into a slower, more cumulative degradation phase where systems are still functioning, but less efficiently, less affordably, and with far less margin for error.

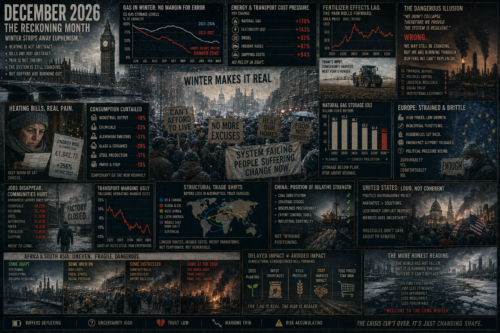

December is the reckoning month because winter strips away euphemism. Gas and heating become visceral. A logistics delay in June was abstract. A heating bill in December is not abstract. If Europe entered winter in decent shape, December is survivable but politically poisonous. If storage, weather, or LNG access are worse than hoped, then December becomes the month of forced behavioral change: curtailed consumption, industrial throttling, emergency support packages, and severe pressure on incumbents.

Oil by December may no longer be printing the most dramatic headlines, but it remains embedded in everything. Diesel costs, freight frictions, backup generation, petrochemicals, and winter distribution keep the pressure on. Urea and broader fertilizer effects continue to work with a lag; the real agricultural consequences often roll forward into the next planting and harvest cycle rather than exploding theatrically in the same month. That lag is one reason policymakers consistently underestimate the danger. They confuse delayed pain with avoided pain.

China ends the year in a relatively stronger geopolitical position if it has managed stocks, coal substitution, and procurement discipline better than competitors. That does not mean it is “winning” in some simplistic way; it means a fragmented crisis tends to favor states with administrative capacity, coercive economic tools, and a willingness to absorb inefficiency for strategic advantage. Europe ends the year strained and brittle. The U.S. ends the year politically louder than economically coherent. Africa ends the year highly uneven: some states opportunistic, some adaptive, some in quiet distress, and a few on the edge of outright instability.

December is also when the biggest analytic temptation appears: to declare that because civilization has not literally fallen over, the system has proved resilient. That would be far too flattering. A more honest reading is that the world may still be standing while quietly burning through buffers—financial, political, logistical, and social—that it cannot replenish indefinitely.

January 2027.

December is the reckoning month because winter strips away euphemism. Gas and heating become visceral. A logistics delay in June was abstract. A heating bill in December is not abstract. If Europe entered winter in decent shape, December is survivable but politically poisonous. If storage, weather, or LNG access are worse than hoped, then December becomes the month of forced behavioral change: curtailed consumption, industrial throttling, emergency support packages, and severe pressure on incumbents.

Oil by December may no longer be printing the most dramatic headlines, but it remains embedded in everything. Diesel costs, freight frictions, backup generation, petrochemicals, and winter distribution keep the pressure on. Urea and broader fertilizer effects continue to work with a lag; the real agricultural consequences often roll forward into the next planting and harvest cycle rather than exploding theatrically in the same month. That lag is one reason policymakers consistently underestimate the danger. They confuse delayed pain with avoided pain.

China ends the year in a relatively stronger geopolitical position if it has managed stocks, coal substitution, and procurement discipline better than competitors. That does not mean it is “winning” in some simplistic way; it means a fragmented crisis tends to favor states with administrative capacity, coercive economic tools, and a willingness to absorb inefficiency for strategic advantage. Europe ends the year strained and brittle. The U.S. ends the year politically louder than economically coherent. Africa ends the year highly uneven: some states opportunistic, some adaptive, some in quiet distress, and a few on the edge of outright instability.

December is also when the biggest analytic temptation appears: to declare that because civilization has not literally fallen over, the system has proved resilient. That would be far too flattering. A more honest reading is that the world may still be standing while quietly burning through buffers—financial, political, logistical, and social—that it cannot replenish indefinitely.

February 2027.

February is about administrative triage. Governments everywhere discover that they are no longer managing growth or even recession. They are assigning priority to collapse. Which sectors get diesel. Which ports get police protection. Which households get heating support. Which fertilizer shipments are escorted. Which currencies get defended. Which lies are still useful.

The U.S. suffers a credibility crisis that becomes social before it becomes constitutional. Dollar depreciation now moves from market abstraction to lived insult: imported goods dearer, fuel savage, Treasury weakness turning every subsidy package into a confidence test, every confidence test into partisan warfare. Rural and exurban America does not need ideological sophistication to grasp that the center is failing. It just needs empty shelves, diesel pain, and the feeling that Washington is asking for obedience while being unable to provide order. The guns matter not because everyone starts a civil war on cue, but because state capacity must now negotiate with an armed and distrustful civilian culture.

Pressure on Russia intensifies in a weirdly convergent way. Europe needs barrels. The Americans need some path to lower global oil without openly rewarding Kremlin maximalism. India wants cheap and stable supply, not messianic Russian chaos. China wants Russian energy but not a total Eurasian bonfire. Even some Gulf actors would prefer a post-Putin arrangement that keeps Russian crude in circulation while reducing random strategic lunacy. So February sees the growth of an unspoken international position: Russia should remain strong enough to pump, weak enough to bargain, and rid of the one man least capable of de-escalatory adaptation.

In China, February is the month when the old start being abandoned by arithmetic. Not always literally. Often familially, quietly, apologetically. Three-generation households become stress chambers. Medication runs out. Heating gets prioritized downward. Calorie allocation becomes brutal in poor families. A society with weak broad safety nets and a collapsing growth machine does not hold up its elderly with slogans. It falls back on family. When family income collapses too, the elderly become the first “nonproductive” mouths to be deprioritized. This is one of the ugliest truths in the whole scenario.

March 2027.

March is when hunger becomes globally legible. Not necessarily because the worst deaths happen that month, but because the indicators stop being deniable. Shipping delays, fertilizer non-application, fuel rationing, failed imports, currency crashes, and local crop stress begin fusing into one visible pattern. Humanitarian agencies are overwhelmed. Rich states start deciding, implicitly or explicitly, that they can save some corridors and not others.

Sub-Saharan Africa, Yemen, Sudan-adjacent zones, parts of the Sahel, Afghanistan, fragile importers in East Africa, and stressed urban populations across multiple developing countries enter a new tier of risk. The problem is not just “not enough food exists.” It is that food arrives too late, costs too much, cannot be milled, cannot be trucked, cannot be refrigerated, cannot be purchased with collapsing currency, or is blocked by insecurity. Diesel is civilization. When diesel goes feral, famine stops being a harvest story and becomes a logistics story.

Russia in March is now thick with coup-rumor fog, succession gossip, factional testing, and strategic ambiguity. The most likely route is not a clean palace coup with brass bands. It is an incremental narrowing of Putin’s real options: harder elite buffering around him, selective information starvation, security reshuffles, “health” rumors, quiet foreign signaling, and perhaps a managed patriotic pretext for transition. The world does not need Russian liberal democracy here. It needs a more transactional sovereign gangster with a calculator.

The U.S. increasingly cannot behave like the hegemon because it cannot afford hegemonic fuel prices with a broken bond market. Emergency releases, maritime protection, jawboning, coercive diplomacy, and financial theater continue, but the underlying fact is now humiliatingly plain: the American system was not built to tolerate sustained $300–$500 oil equivalents without either authoritarian improvisation, social fracture, or both. Europe can become poorer. America becomes meaner and stranger.

April 2027.

April is the first month where some places start seeing localized mortality spikes that are impossible to euphemize. Clinics lose power. Vaccine cold chains fail. Maternal care degrades. Water pumping becomes erratic. Cholera and diarrheal disease turn food insecurity into death multiplication. You do not need literal starvation to kill astonishing numbers of people once health systems are wobbling.

China’s contraction now stops looking cyclical and starts looking civilizationally humiliating. Industrial zones are partly silent. Youth unemployment is no longer even the right category because whole local ecologies of work have vanished. The state can still repress dissent, but repression does not create calories. Urban food queues, ration coupons, and informal barter begin to matter more. Internal migration controls may harden because Beijing cannot allow total free movement of desperate populations toward cities already unable to absorb them. The old in rural China suffer worst of all: reduced remittances, weak care networks, failing township medicine, and social invisibility.

April is also when elite appetite for a Russian reset reaches its highest rational intensity. The logic is brutally simple. If Russia could export more oil under a leadership transition that preserved state continuity, partially quieted the war machine, and reopened some channels of commerce, then nearly every major power bloc has a reason to tolerate that outcome. Not love it. Tolerate it. Putin increasingly becomes a scarcity premium with a face.

Europe by now is exhausted but functional. Its great advantage is still administrative grimness. It can ration, subsidize, coordinate, and moralize at scale. It cannot avoid pain, but it can distribute it in a semi-organized way. It does not “solve” the crisis. It survives it socially better than the U.S. The price is political radicalization, industrial loss, and a lot of quiet de-development masked as transition.

May 2027.

May is when the ephemeral trend layer gets weird. You asked for that, and it matters because societies under duress develop grotesque surface behaviors.

This is the month of “salvage chic,” black-market domesticity, fuel-minimal status signaling, conspicuous thrift among the affluent, and a moralized aesthetics of endurance. Luxury doesn’t vanish, it mutates. The rich brag about backup systems, local procurement, protected transport, private wells, garden walls, and secure diesel the way they once bragged about yachts. Lifestyle media becomes apocalypse-adjacent. Influencers rediscover lentils as if they invented peasants. Governments push “community resilience” campaigns because saying “we are triaging collapse” polls badly.

In the U.S., militia-coded localism, church pantry patriotism, generator masculinity, and paranoid county-level self-organization spread culturally far faster than any actual coherent secession. Not Mad Max. Something more American and more embarrassing: county fairs with ammunition tables and diesel gossip, school board meetings as proto-emergency councils, suburban Facebook groups becoming food-security rumor exchanges with assault rifles in the background.

In China, surface culture goes gray. Weddings shrink. Meat disappears from celebratory normalcy. Street life dulls. Status moves toward access, not display: who can source rice, medicine, transport, safe apartments, cadre protection. The elderly become not just materially endangered but symbolically awkward, visible reminders that the social contract of rising prosperity has broken. A society that can no longer promise upward motion becomes cruel to dependency.

Globally, by May, the food emergency is now beyond “warning.” Death totals are climbing, but the larger figure is the number of people in severe acute distress. Under your scenario, 200–350 million people in very severe food insecurity by this point is entirely plausible, with mortality already in the millions if aid and trade routes have badly degraded.

June 2027.

June is the anniversary month, which means political systems become obsessed with narrative control. Everyone wants to claim the worst is passing. Everyone lies.

If Putin is still formally in place by June, he is likely already a reduced sovereign, boxed in by factions, increasingly ceremonial in some domains and hyper-destructive in others. If he has been displaced, June is the month of the “transitional patriot”: some hard-faced security figure or elite coalition front-man promising continuity, honor, order, and the normalization of exports. Markets would not celebrate from joy. They would collapse onto the new arrangement with the enthusiasm of starving rats finding grain. Russian oil re-entry at scale would be treated globally as a moral obscenity and an economic necessity at the same time. That is the actual adult truth here.

The dollar by June has lost not just value but mystique. It can still function, of course; reserve currencies do not vanish like Snapchat filters. But its aura is damaged. Treasuries are no longer automatic sanctuary. Allies diversify faster. Bilateral settlement experiments proliferate. Commodity exporters demand harder terms. The U.S. discovers that reserve-currency decline is not an academic debate but a national temperament problem. Americans are not culturally designed for imperial downshifting. They are designed for denial, anger, and weird reinventions.

June also brings heat, which means power demand, water stress, and food spoilage risk rise simultaneously. Developing countries without reliable cooling and grid stability get mauled. This is where hunger kills children fast and the old quietly. A crop failure is one thing. A hot distribution environment with weak power, weak water, weak medicine, weak fuel, and weak state legitimacy is a death machine.

July 2027.

July is when societies begin showing malnutrition behavior more visibly. That sounds clinical, but it matters. School attendance drops. Labor productivity falls. Minor infection becomes major. Irritability, passivity, theft, domestic violence, and local political violence all rise. Hungry societies are not just sad. They are cognitively and socially damaged.

China in July is very dark under this scenario. The question of “what happens to the old” gets a cruel answer: many die earlier than they otherwise would, not always through headline famine but through cascading neglect. Pension insufficiency, family collapse, lack of transport to clinics, ration discrimination, under-heating, and untreated chronic disease do the work. There may also be selective institutional concealment, with local cadres suppressing mortality data to avoid panic or punishment. Chinese hunger in 2027 would be a mixture of modern scarcity and very old shame.

In the developing world, July is where the death curve can steepen sharply if spring planting was degraded and humanitarian response remains underpowered. I still would not throw out “half a billion dead” by end-year as the central estimate. That is near-civilizational extermination scale. But half a billion people facing extreme food stress or near-famine conditions under the harsher branch? Yes, very conceivable. Actual deaths by late 2027 in the high single-digit millions to perhaps tens of millions becomes thinkable if multiple regions fall into disease-plus-hunger compounding.

In the U.S., heat plus fuel pain plus fiscal failure plus weakened federal legitimacy create ugly local episodes. Not total national collapse. Something more fragmented and American: utility unrest, convoy theft, ad hoc deputization, politicized National Guard deployments, and constant rhetorical escalation between center and periphery. The country doesn’t neatly “break.” It frays along lines of infrastructure, trust, and who can still compel whom.

August 2027.

August is the month of international moral exhaustion. The donor states are tired. Their publics are tired. Their fiscal positions are worse. The number of crises exceeds the emotional and budgetary bandwidth of the rich world. This is when abandonment becomes normalized.

A post-Putin or diminished-Putin Russia now moves to extract maximum rehabilitation value from its oil. Not full redemption, obviously. More like a sordid bargain: more barrels, fewer tantrums, selective ceasefire posture, anti-chaos messaging, limited inspection regimes, backchannel sanctions easing, maybe some frozen-asset games. No one likes it. Everyone does it. The world rediscovers in disgust that petroleum is a moral solvent.

Europe in August starts thinking beyond survival and toward structural repositioning. Permanent demand destruction in some industries, accelerated nuclear reconsideration in some capitals, emergency agro-policy shifts, and stronger state direction of infrastructure begin to look less temporary. Europe does not come out clean. It comes out more dirigiste, poorer, meaner on migration, and less naïve about strategic dependency.

China’s internal legitimacy crisis deepens, but not necessarily in a liberalizing direction. The state’s instinct will be tighter control, tighter information, harsher anti-hoarding enforcement, politically selective relief, and patriotic language about endurance. Hunger often strengthens coercion before it destroys it.

September 2027.

September is when the next harvest expectations either save the world from the worst branch or confirm that it is still descending. If fertilizer use remained badly suppressed, irrigation impaired, and rural finance wrecked, then September is the month planners realize 2028 is also contaminated. That is the nightmare: not a single famine pulse, but a rolling degradation of productive capacity.

The U.S. by now may have partially stabilized fuel availability through ugly measures, but at the cost of deeper damage to fiscal credibility, institutional trust, and class peace. A country that once outsourced discomfort to bond markets and empire is now being forced to metabolize it domestically. That changes its politics in lasting ways. More coercive, more conspiratorial, less governable.

Russia in September is either in managed succession or permanent shadow transition. The crucial thing is that global pressure was never really “liberal anti-Putin morality” alone. It was algorithmic in the coldest sense: the world’s energy system was assigning enormous negative value to his continued discretionary chaos. Once that negative value outweighed the elite costs of transition, transition became rational.

Global food mortality is now obscene. I would model by September something like 300–500 million people in acute or worse food insecurity under the hardest branch, but deaths still well below that number. Death tolls in the several millions and climbing steeply are plausible. The horror is scale without clean countability.

October 2027.

October is the bureaucratization of catastrophe. Emergency conditions that were improvised earlier in the year become permanent structures: ration systems, priority fuel allocations, guarded grain movements, strategic import monopolies, local movement restrictions, emergency public works, and selective debt standstills. This is where collapse becomes government-shaped.

Trendwise, autumn 2027 becomes culturally obsessed with durability, hardness, calorie density, and anti-fragile identity. Soft luxury is tacky now. Heaviness is in. Workwear, repair culture, preserved foods, local militancy, hard religion, maternal mutual-aid networks, funerary normalization, and a new aesthetics of stern competence all spread. Societies under prolonged scarcity stop worshipping abundance and start worshipping survivability. It is spiritually narrowing.

In China, older people now disappear from public life in greater numbers. Some die. Some stay home. Some are hidden. Some are simply no longer affordable to include in social rituals. A collapsing economy without robust universal protection turns aging into an accusation. It is bleak as hell.

November 2027.

November is when the world starts doing retroactive moral accounting while the killing is still ongoing. Commissions, leaks, elite memoir-positioning, blame campaigns, sanctions redesign talks, reserve-system panels, food-security summits, all the usual civilization-after-a-bender behavior. People begin competing to have been right.

The U.S. is still dangerous, still armed, still economically enormous, but no longer reassuring. Dollar depreciation and Treasury distrust have forced a humiliating recognition that domestic cohesion was a hidden pillar of financial supremacy. Once that cohesion cracks, market plumbing becomes geopolitical psychology. The country remains powerful, but it no longer feels in command of cause and effect.

Russia, if reconfigured, is now treated the way the world treats many ugly but useful regimes: publicly loathed, privately courted. More oil flows. More insurance pathways reopen. Prices ease from the very worst levels, but not cleanly enough to undo the year’s damage. Too late for millions.

December 2027.

December judges everybody. By now everyone hates the United States more than ever in human history. In the United States there is no realistic future left for the existing political system, but we can not conceive of how this would resolve itself. Neither the Republican or Democratic party apparatus can meaningfully persist. New ideological frameworks must emerge and by the look of this polarization and division will increase, gridlock will increase, violence and disfuntion is likely to follow.

The best-case branch by this point is that Russian export normalization, partial energy repricing, adaptation in Europe, and some stabilization in U.S. logistics prevent a true 2028 planetary free-fall. The worst-case branch is that 2027 has already irreversibly damaged agricultural capacity, public finance, and human health across enough regions that 2028 inherits a starvation overhang.

China ends 2027 poorer, colder, hungrier, and more authoritarian, with its elderly disproportionately dead, abandoned, or medically degraded. The U.S. ends 2027 fiscally diminished, domestically uglier, and less able to pretend that money abstraction can outrun physical scarcity. Europe ends 2027 scarred but comparatively coherent. Russia ends 2027 either under new management or under a hollowed-out Putin whose continued personal rule has become almost theatrical. Large parts of the developing world end 2027 in grief.

So, no, I would not project “half a billion dead” as the central headline. That is probably too high for deaths by December 2027 unless several additional black swans pile in. But I would write, without flinching, something like this:

By end-2027 under this scenario, 400–600 million people could plausibly be in acute food distress or worse, with global excess deaths from hunger, disease, conflict spillover, and state failure potentially reaching the high single-digit millions and, in the harsher branch, edging into the tens of millions.

That is already civilization-scale shame. You do not need to inflate it into a comic-book number to make it monstrous.

Concluding – Closure of Hormuz, Free Flow Of Oil is Long Term Unacceptable

Fine. Here’s the less civilized version.

A prolonged Hormuz shutdown beyond April or May 2026 would be an obscenity of incompetence. Not a “challenge.” Not a “stress test.” Not a “complex geopolitical moment.” It would mean the people supposedly running major states and institutions had looked straight at one of the most obvious choke points in the global system and decided to behave like vain, senile, press-release-addicted frauds while the fuel, fertilizer, and shipping backbone of modern life started to seize. Roughly 20 million barrels per day of oil exports were moving through Hormuz in 2025, about a quarter of global seaborne oil trade. The plausible bypass is only 3.5–5.5 million barrels per day. LNG exposure is roughly one-fifth of global trade. Around one-third of global seaborne fertilizer trade passes through that corridor, heavily concentrated in urea. This is not subtle. This is not a mystery. A moderately literate intern with a map and a calculator can understand the scale of the problem.

Going in with a military intent was an act of sheer incandescent incompetence, if not basement back-elley level gangster cynicism. If politicians still let this drag on, the verdict is simple: they are idiots, cowards, narcissists, likely some nauseating combination of all three. Because once you know those numbers, you also know the consequences. You know diesel tightens freight. You know freight tightens food. You know LNG stress wrecks heating, power, and industry. You know fertilizer disruptions do not just make farmers grumble; they degrade planting decisions and next-season yields. You know poorer importing countries do not have magical resilience reserves hidden in a drawer. And if you know all that and still spend month after month producing summits, “frameworks,” temporary ceasefires, and the usual diplomatic landfill of statements by “concerned leaders,” then you are not managing events. You are letting civilization run on fumes because you prefer theatrical impotence to decisive risk.

What makes it worse is that this would not even be a case of noble sacrifice. It would be failure without grandeur. The world would not collapse in one dramatic bang. It would rot by invoice. Fuel surcharges. Insurance spikes. Refinery strain. Procurement panic. Subsidy blowouts. Industrial shutdowns. Food inflation. Layoffs. Currency stress. Political rage. That is how systems actually die: not with movie explosions, but with exhausted families, delayed cargoes, bad harvest math, and governments pretending that a spreadsheet full of emergency measures is the same thing as control. Any politician who cannot grasp that a months-long Hormuz disruption means the coupling of oil stress, gas stress, and fertilizer stress is too stupid to be trusted with a stapler, let alone a state.

And spare me the usual sanctimonious sludge about “difficult trade-offs.” Yes, the trade-offs are difficult. That is why adults exist. If leaders cannot keep one of the central energy arteries of the world open, or force a settlement, or build a genuinely credible emergency regime fast enough to stop the bleeding, then they deserve contempt, not sympathy. Because the people who pay for elite dithering are always the same: import-dependent poor countries first, ordinary households second, industrial workers third, and only then the donor-class cretins who spent the spring congratulating themselves on nuance while nitrogen, diesel, and gas quietly lined up to mug the global economy.

The blunt truth is this: beyond April or May 2026, a shutdown of Hormuz is no longer a temporary disruption. It becomes proof that the political class of multiple major powers is functionally unfit. Unfit because they cannot prioritize. Unfit because they confuse posturing with statecraft. Unfit because they think history will forgive them for acting like commentators while the physical substrate of the world economy starts cracking. This is running politics like a 4 year old managing insects with a magnifying glass. Oil is not optional. Gas is not optional. Urea is not optional. Shipping confidence is not optional. Anyone in power who behaves otherwise should be spoken of with the level of respect usually reserved for drunks trying to perform surgery. I have much less flattering metaphors.

The real obscenity is that they would all know this, and still keep stalling. Instead they send their imbecile sociopathic son in law to close deals, and do absurd, abstract and meaningless transactions that generate billions that in any practical reality become unspendable. Spend billions where, when the entire world will want to hang you upside down from a bridge? That is what makes this banale pettiness infuriating. Not ignorance. Not tragedy. Knowing negligence. A whole class of overpaid, overprotected, media-trained mediocrities watching the molecules stop moving and still talking like this is a reputational management exercise, or a brochure opportunity. They should be ashamed, but shame requires an intact moral nervous system, and that seems to be in shorter supply than diesel. One misses Guillotines at this stage, but if all this goes off the rails we might by 2028 or later see much much worse than mere Guillotines.